| |

March 28 - April 1, 2022 Recap Stocks Rally Third WeekBroad Market Stocks Inch Higher For the Week… ISM Manufacturing Surprises Lower Real Estate Rebounds Treasury Prices Drop | |

The Latest from @CeteraIM | |

Economic CalendarMonday, April 4 Tuesday, April 5 Wednesday, April 6 Thursday, April 7 Friday, April 8 | |

| |

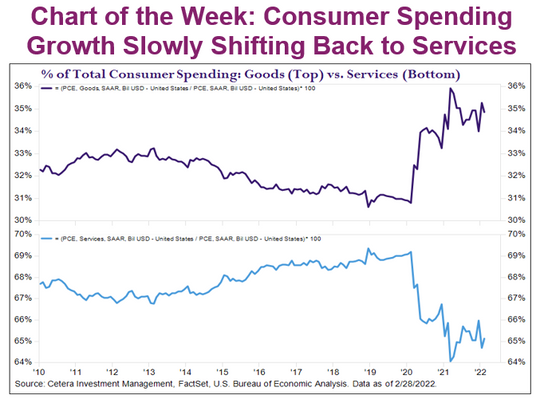

Consumer spending habits changed during the pandemic. Growth in consumer spending was stronger for goods than services because of pandemic restrictions. We anticipate that consumer spending growth will be stronger for services going forward as the impact on the economy from the omicron variant continues to fade. | |

| |

This report is created by Cetera Investment Management LLC. For more insights and information from the team, follow @CeteraIM on Twitter. About Cetera® Investment Management About Cetera Financial Group Disclosures The material contained in this document was authored by and is the property of Cetera Investment Management LLC. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by affiliated and non-affiliated registered investment advisers. Your registered representative or investment adviser representative is not registered with Cetera Investment Management and did not take part in the creation of this material. He or she may not be able to offer Cetera Investment Management portfolio management services. Nothing in this presentation should be construed as offering or disseminating specific investment, tax, or legal advice to any individual without the benefit of direct and specific consultation with an investment adviser representative authorized to offer Cetera Investment Management services. Information contained herein shall not constitute an offer or a solicitation of any services. Past performance is not a guarantee of future results. For more information about Cetera Investment Management, please reference the Cetera Investment Management LLC Form ADV disclosure brochure and the disclosure brochure for the registered investment adviser your adviser is registered with. Please consult with your adviser for his or her specific firm registrations and programs available. No independent analysis has been performed and the material should not be construed as investment advice. Investment decisions should not be based on this material since the information contained here is a singular update, and prudent investment decisions require the analysis of a much broader collection of facts and context. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. The opinions expressed are as of the date published and may change without notice. Any forward-looking statements are based on assumptions, may not materialize, and are subject to revision. All economic and performance information is historical and not indicative of future results. Investors cannot directly invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. Glossary The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The S&P 500 is an index of 500 stocks chosen for market size, liquidity and industry grouping (among other factors) designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. The NASDAQ Composite Index includes all domestic and international based common type stocks listed on The NASDAQ Stock Market. The NASDAQ Composite Index is a broad based index. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe and is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 3000 Index measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S. equity market. The Russell Midcap Index measures the performance of the mid-cap segment of the U.S. equity universe and is a subset of the Russell 1000 Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Bloomberg Barclays US Aggregate Bond Index, which was originally called the Lehman Aggregate Bond Index, is a broad based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government–related and corporate debt securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency) debt securities that are rated at least Baa3 by Moody’s and BBB- by S&P. Taxable municipals, including Build America bonds and a small amount of foreign bonds traded in U.S. markets are also included. Eligible bonds must have at least one year until final maturity, but in practice the index holdings have a fluctuating average life of around 8.25 years. The Bloomberg Barclays US Corporate High Yield Index measures the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high yield if the middle rating of Moody's, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging market debt. Payment-in-kind and bonds with predetermined step-up coupon provisions are also included. Eligible securities must have at least one year until final maturity, but in practice the index holdings has a fluctuating average life of around 6.3 years. The Bloomberg Barclays US Municipal Bond Index covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds. Eligible securities must be rated investment grade (Baa3/BBB- or higher) by Moody’s and S&P and have at least one year until final maturity. The MSCI EAFE Index is designed to measure the equity market performance of developed markets (Europe, Australasia, Far East) excluding the U.S. and Canada. The Index is market-capitalization weighted. The MSCI Emerging Markets Index is designed to measure equity market performance in global emerging markets. It is a float-adjusted market capitalization index. The Bloomberg Commodity Index is a broadly diversified index that measures 22 exchange-traded futures on physical commodities in five groups (energy, agriculture, industrial metals, precious metals, and livestock), which are weighted to account for economic significance and market liquidity. No single commodity can comprise less than 2% or more than 15% of the index; and no group can represent more than 33% of the index. The S&P GSCI Crude Oil Index is a sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark for investment performance in the crude oil market. The S&P GSCI Gold Index, a sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark tracking the COMEX gold futures market. The U.S. Dollar Index is a weighted geometric mean that provides a value measure of the United States dollar relative to a basket of major foreign currencies. The index, often carrying a USDX or DXY moniker, started in March 1973, beginning with a value of the U.S. Dollar Index at 100.000. |

Weekly Recap | April 4, 2022

April 05, 2022